Table of Contents

The Architecture of Fragmentation: Geopolitics and the Structural Emergence of Economic Balkanization

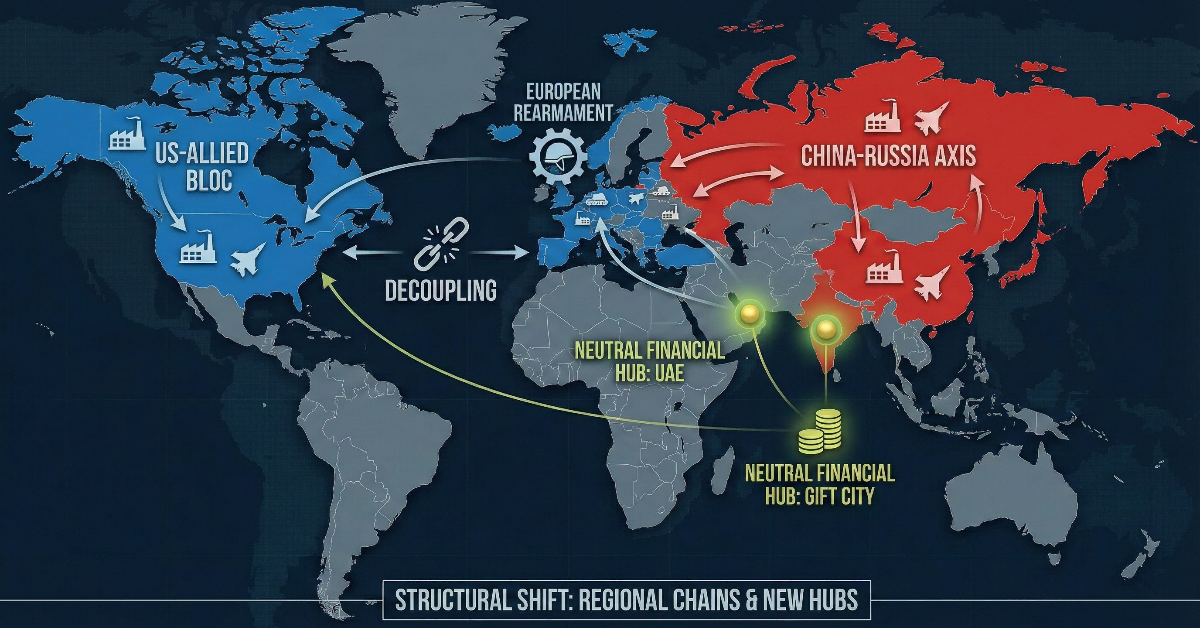

The global economic landscape in 2026 is no longer defined by the friction-less ideals of the late twentieth-century globalization. Instead, a new era of “Economic Balkanization” has taken root, characterized by the deliberate decoupling of major powers, the prioritization of national security over market efficiency, and the rise of a multipolar architecture that rewards strategic autonomy. The move away from open globalization toward regional supply chains and strategic alliances is not a temporary disruption but a fundamental structural shift. This report analyzes the mechanisms of this realignment, focusing on the financial decoupling of the United States and China, the transformation of defense into a primary industrial driver, the tactical and structural shifts in global trade routes, and the necessary adjustments for the sophisticated investor in this fragmented reality.

The Multipolar Portfolio: Strategies for a Decoupling Financial Order

The traditional dominance of the U.S. dollar-centric financial system is facing its most significant challenge since the Bretton Woods agreement. In 2026, the global financial order is characterized by an “unmanaged decoupling” between the U.S. and Chinese systems, a process accelerated by the aggressive use of financial sanctions and the pursuit of technological sovereignty. While the U.S. dollar remains the world’s primary reserve currency, participating in approximately 90% of all currency trading, its share of global reserves has descended to roughly 58%, down from over 70% in previous decades. This erosion is not a sign of the dollar’s immediate collapse but rather the emergence of a multi-currency world where regional hubs provide the necessary liquidity and “sanctions-neutral” infrastructure for global trade.

The Rise of Neutral Intermediaries and Financial Hubs

As the U.S. and China diverge, a group of neutral intermediaries—India, the United Arab Emirates (UAE), and Brazil—has successfully positioned itself to capture the resulting capital flows. These nations leverage their geopolitical “multi-alignment” to serve as bridges between competing blocs, offering specialized financial environments that minimize the risks associated with great-power rivalry.

India has emerged as a central anchor in this new architecture, particularly through the development of the Gujarat International Finance Tec-City (GIFT City). Conceived as an equivalent to Singapore or Dubai, GIFT City has become India’s first operational smart city and an international financial services center (IFSC) that attracts global capital seeking exposure to the Indian growth story without the traditional offshore intermediation costs. By early 2026, GIFT City hosted over 1,034 registered entities, including 38 major global banks such as HSBC, J.P. Morgan, and Barclays, with total banking assets surpassing $100 billion. The competitive advantage of this hub is rooted in an aggressive regulatory and tax structure.

| Financial Hub Metric (2026) | GIFT City (India) | DIFC (UAE) | Singapore (Baseline) |

| Corporate Income Tax | 10-year 100% Exemption | 0% (in specific zones) | 17% |

| GST/VAT on Transactions | 0% | 5% (with exemptions) | 9% |

| Operating Cost Index | 20% of Global Avg | 65% of Global Avg | 100% |

| Banking Assets (USD) | $100.14 Billion | $200+ Billion | $2+ Trillion |

| Primary Strategic Role | Emerging Market Gateway | Sanctions-Neutral Liquidity | High-Wealth Management |

The UAE has similarly reinforced its position as a global financial hub by modernizing its capital market regulations. On January 1, 2026, two federal decree laws came into effect, expanding the independence of the Capital Markets Authority and increasing its enforcement powers to align with international standards set by the IMF and IOSCO. Furthermore, the Dubai International Financial Centre (DIFC) introduced new crypto regulations on January 12, 2026, shifting the responsibility for token suitability assessment onto firms and abolishing the mandated “approved list” of tokens. This move fosters a “digital-native” environment that appeals to firms seeking to avoid the increasingly rigid regulatory structures of the U.S. and EU.

BRICS+ and the Mechanics of De-Dollarization

The expansion of the BRICS bloc to “BRICS Plus”—including Egypt, Ethiopia, Iran, and the UAE—represents a concerted effort to create a viable counterweight to the Western-dominated global system. A central objective of this group is the reduction of reliance on the U.S. dollar, a process known as de-dollarization. While a single, unified BRICS currency remains a distant prospect due to the massive economic disparities between members like China and Brazil, the group has made significant strides in strengthening trade in local currencies.

The “BRICS Pay” system, a decentralized payment messaging platform, now facilitates transactions in local currencies, effectively bypassing the U.S.-led SWIFT system. In Russia, the share of national currencies in settlements with “friendly” partners like China, India, and Egypt has reached approximately 90% as of late 2025. China’s approach within BRICS+ remains pragmatic, seeking to build a cooperative framework and provide financing through the New Development Bank and the Asian Infrastructure Investment Bank rather than directly antagonizing the West. However, the U.S. has responded to these trends with heightened aggression; the Trump administration has threatened 100% tariffs on imports from BRICS member states that actively pursue de-dollarization, framing the issue as an ideological battle for global financial hegemony.

Brazil’s Neutrality Trap

Brazil exemplifies the challenges of maintaining neutrality in a balkanized world. Under President Luiz Inácio Lula da Silva, Brazil has pursued a “multi-alignment” strategy, balancing ties with Washington and Beijing while elevating its role in BRICS and the G20. China is now Brazil’s largest trading partner, consuming nearly half of its beef exports and investing billions in strategic sectors such as ports, energy, and logistics terminals. This deepening commercial dependence on China, however, creates sovereignty risks and leaves Brazil vulnerable to U.S. pressure. In 2025, the U.S. briefly levied punitive 40% tariffs on Brazilian imports, a move that was only partially withdrawn due to the U.S.’s own need for Brazil’s rich deposits of critical minerals and rare earths. As the 2026 elections in Brazil approach, the risk remains that the country may eventually be forced to choose sides as the room for maneuver between the two superpowers diminishes.

Defense as an Infrastructure Play: The Fiscal Impact of European Rearmament

The end of the “peace dividend” that characterized the post-Cold War era has led to a fundamental pivot in European defense policy. Rearmament is no longer viewed as a temporary response to the conflict in Ukraine but as a permanent, structural driver of industrial demand and a core component of the EU’s industrial strategy. The “Readiness 2030” plan and the “ReArm Europe Plan” aim to mobilize up to €800 billion for defense investments by the end of the decade, reshaping the relationship between the state and the defense industry.

The Industrial Strategy of Rearmament

European rearmament is being structured as an “infrastructure play,” where military spending is designed to yield considerable economic spillovers into the civilian high-tech sector. The focus has shifted from traditional crewed platforms to autonomous systems, robotics, applied AI, and sovereign space access. For instance, the UK’s 2025 Defense Review proposed a spending goal of 40% on reusable autonomous systems and 40% on “consumables” like drones and missiles, with only 20% reserved for traditional crewed systems.

| Defense Investment Pillar (Readiness 2030) | Primary Technological Focus | Economic/Industrial Objective |

| Autonomous Systems & Robotics | AI-driven drones, land/sea bots | Augmenting scarce manpower |

| Applied AI & Software | Advanced algorithms, ML | Achieving “Mass” on the battlefield |

| Sovereign Space Infrastructure | Satellite constellations (e.g., OneWeb) | Secure comms & independent positioning |

| Hypersonic Weapon Systems | Modern missile tech, propulsion | Strategic deterrence & R&D leadership |

The fiscal mechanism for this rearmament includes the “Security Action for Europe” (SAFE), a financial instrument providing up to €150 billion in long-maturity loans (up to 45 years) to Member States. These loans facilitate common procurement, which is essential for achieving the economies of scale needed to strengthen the European Defense Technological and Industrial Base (EDTIB) and reduce unit costs through standardization.

Macroeconomic and Fiscal Consequences

The long-term fiscal impact of this spending is a subject of intense analysis. Macroeconomic simulations using the QUEST model estimate that a linear increase in defense spending by 1.5% of GDP across the EU could raise real GDP by 0.5% by 2028. However, this growth is accompanied by an increase in the EU government debt-to-GDP ratio of approximately 2 percentage points. The “peace dividend” trough of 1.1% of GDP in 2014 has given way to a median rise of 0.6% of GDP in just two years among European NATO members, with 20 of 28 members reaching the 2% NATO target by 2024.

| Fiscal Metric: European Rearmament Impact (2028 Projection) | Impact Value |

| Incremental Real GDP Growth (EU-wide) | +0.3% to +0.6% |

| Incremental Public Debt-to-GDP Ratio | +2.0 percentage points |

| High Productivity Scenario (20% Capital Share) | +0.2 pps additional GDP |

| Average Defense Spending Multiplier | 0.6 to 0.8 |

The primary risk to this strategy is the fragmentation of the European defense market. Without pooled procurement, additional demand mainly drives up prices and creates rents for established national contractors. The proposed European Defence Mechanism (EDM) seeks to address this by centralizing procurement and creating a defense single market that prohibits state aid and national preferences. This would allow for a halving of unit costs for certain platforms, such as self-propelled howitzers, by scaling up production capacity.

Tariff Front-Running and the Structural Re-Routing of Global Trade

The reconfiguration of global trade in 2026 is driven by a combination of tactical maneuvers and permanent structural realignments. Governments are increasingly using tariffs not just for revenue, but as strategic tools of industrial policy and geopolitical pressure. This has led to the phenomenon of “tariff front-running” or “export front-loading,” where firms accelerate shipments to avoid impending trade barriers, creating temporary volatility that obscures long-term shifts in trade corridors.

Tactical Volatility: The Front-Loading Effect

In 2025, Chinese exports to the U.S. surged ahead of new tariff increases, with nominal export flows in December 2024 alone being $6.6 billion higher than the previous year—a 15.6% increase. This front-loading creates a “bullwhip effect” in global logistics, where a period of intense activity is followed by a sharp slowdown. By November 2025, U.S. container imports fell 7.8% year-over-year, with imports from China dropping by nearly 20% as the front-loaded inventory was consumed and new tariffs took effect.

This tactical behavior creates significant pressure on trade infrastructure. Too much capacity chasing too little volume on core Asia-U.S. lanes results in blank sailings and spot rate volatility. For businesses, this necessitates a “hard reset” of demand planning, moving away from single-point forecasts toward a scenario-based mindset that accounts for policy-driven volatility.

Structural Realignment: Next-Generation Trade Hubs

While front-loading is temporary, the structural shifts in trade routes are permanent. Geopolitical distance—the degree of political alignment between nations—now has a measurable impact on trade: a 10% increase in geopolitical distance reduces bilateral trade by 2%. This has led to the rise of “friendshoring” and the emergence of next-generation trade hubs that serve as alternatives to the U.S.-China corridor.

| Next-Gen Trade Hub (2025/26 Ranking) | Key Advantage | Strategic Shift |

| UAE (#1) | Multimodal powerhouse; DIFC hub | Linking Asia-ME-Europe South-South trade |

| Vietnam (#2) | Surging exports; new U.S. tariff deal | Central node for Asia’s manufacturing re-route |

| Malaysia (#3) | Top 10 global port (Klang) | High-tech manufacturing & regional logistics |

| Saudi Arabia (#4) | Sharpest rise in potential (+11 spots) | Expanding non-oil exports via low tariffs (~4%) |

| Mexico (#12) | Proximity to U.S.; USMCA alignment | Nearshoring acceleration for North America |

Vietnam’s leap to the #2 spot is particularly significant, buoyed by a landmark tariff deal signed with the U.S. in mid-2025 that cements its role as the primary alternative for manufacturing re-routed from China. Mexico also continues to benefit from the USMCA 2026 review process, which strengthens regional integration and nearshoring corridors.

The Middle Corridor and Chancay Port: New Arteries of Trade

Two specific logistical developments are redrawing the map of Eurasian and South American trade. The Middle Corridor (Trans-Caspian International Transport Route or TITR) has gained permanent momentum as a sanctions-compliant alternative to the Northern Corridor through Russia. Transit volumes on this route are forecast to quadruple by the end of the decade, with cargo handled via Azerbaijan Railways alone growing 6% in 2025 to over 2.6 million tons.

| Middle Corridor Projections (TITR) | 2024 Actual | 2025 Forecast | 2027 Forecast |

| Total Cargo Volume (Metric Tons) | 4.5 Million | 5.2 Million | 10.0 Million |

| Growth Rate (YoY) | 62% | 15% | 100% (vs 2025) |

| Container Volume (TEU) | ~60,000 | 96,000 | 200,000+ |

| Strategic Drivers | Red Sea risks; Russia sanctions | Trade policy shifts | Regional multimodal joint ventures |

Simultaneously, the Port of Chancay in Peru has become the “central nerve” of China-Latin America trade. This $3.5 billion Chinese-financed mega-port, fully operational as of November 2024, allows deepwater vessels too large for the Panama Canal to bypass U.S. and Mexican ports. The port cuts shipping times from South America to Shanghai from 40 days to 23 days, reducing logistics costs by 20% and creating a Chinese-operated infrastructure that is immune to U.S. maritime pressure. This port is the anchor of a 2,600-mile bi-oceanic corridor that connects Brazil’s agricultural heartland directly to the Pacific.

Adjusting the Investor Playbook: Navigating the Balkanized Economy

The fragmentation of the global economy into geopolitical blocs requires a fundamental shift in asset allocation and risk management. Traditional “buy and hold” strategies in broad indices are being challenged by the divergent performance of regional markets and the prioritization of “national security” themes.

Thematic Focus: AI, Energy, and Multipolarity

For 2026, major research institutions have identified four key themes for the multipolar world: AI Diffusion, the Future of Energy, the Multipolar order, and Societal Shifts. The “Multipolar World” theme was the top-performing category in 2025, encompassing stocks related to critical minerals, defense spending, and tech localization.

AI adoption has moved from a software curiosity to an infrastructure imperative. The surge in global energy demand—projected to rise by 10% per year in the U.S. alone for the next decade—is driven by data centers, leading to a “nuclear renaissance” and a focus on power grid growth. Investors are increasingly looking at “AI enablers” and companies providing the low-cost power supply necessary for the AI boom.

Tactical Asset Allocation and Portfolio Defense

In an environment of sticky inflation and high policy uncertainty, active management and diversification are critical. Multi-asset strategies are favoring U.S. equities for their structural profitability but are complementing them with overweight positions in “geopolitically near” emerging markets like India, Taiwan, and South Korea, which are essential nodes in the global AI value chain.

| Asset Class Strategy (2026) | Recommendation | Strategic Logic |

| Equities | Selectively Overweight Tech/Defense | AI monetization & permanent defense demand |

| Fixed Income | Favor Short-to-Intermediate Duration | Benefit from Fed easing; avoid fiscal risk |

| Commodities | Long Gold & Critical Minerals | Hedge against inflation & resource weaponization |

| Alternatives | Event-Driven & Market Neutral | Capture alpha in volatile regional markets |

| Portfolio Defense | Low-Volatility Equities & Options | Mitigate downside from trade policy shocks |

Active ETFs have gained significant traction, particularly those focusing on foreign equities and offering fee waivers, such as the T. Rowe Price Active Core International Equity ETF (TACN), which charges zero fees through early 2027. However, investors must be wary of “NAV erosion” in derivative-heavy income strategies and the potential for regulatory scrutiny of products with high “return of capital” components.

The Digital Frontier: RWA Tokenization

One of the most significant shifts for sophisticated investors is the move toward Real-World Asset (RWA) tokenization. Regulatory hubs like GIFT City and the DIFC are leading the way in creating frameworks for the digital delivery of registered funds and the tokenization of private equity. While the UAE is moving toward firm-led token suitability, the U.S. has passed the GENIUS Act (July 2025), creating a comprehensive federal framework for stablecoins. This allows for “Genius Act compliant” stablecoins, such as the USD1, to be backed by U.S. Treasuries and traded within regulated frameworks, bridging the gap between traditional finance and the decentralized Web3 world.

The Convergence of Risk and Opportunity

The transition toward Economic Balkanization is characterized by the replacement of global efficiency with regional resilience. The data from 2025 and 2026 confirms that this shift is not merely political rhetoric but is reflected in trillions of dollars of infrastructure investment, the reconfiguration of trade routes, and the creation of alternative financial architectures.

The emergence of the “multipolar portfolio” requires investors to recognize that “geopolitical distance” is now as important a metric as “price-to-earnings ratios.” The rise of India’s GIFT City and the UAE’s DIFC as neutral intermediaries provides necessary relief valves for global capital, while the Port of Chancay and the Middle Corridor represent the new physical reality of trade. Similarly, the transformation of European defense spending into a permanent industrial engine creates a multi-decade demand signal for high-tech manufacturing.

Ultimately, the successful organization or investor in this era will be the one that can operate within a “scenario mindset,” acknowledging that the “unmanaged decoupling” of the major powers will continue to create pockets of extreme volatility alongside unprecedented opportunities for those who can provide the infrastructure, energy, and security that the fragmented world demands. The age of laissez-faire is over; the age of the strategic player has begun.